Please refer to important disclosures at the end of this report

1

Government of India is divesting 9,33,12,000 shares (9.33% stake) in MMTC. It

has set a floor price of `60 (72% discount to CMP) for the OFS. We recommend

investors to AVOID subscribing to shares due to expensive valuation.

Company overview

MMTC was established in 1963 and is the largest trading company in India and

one of the major trading companies in Asia. It is a Mini Navratna compan

y

focusing on trading of commodities ranging form minerals to agro commodities.

It deals in Precious metals, fertilizers, Coal and Hydrocarbons, Metals, Agro

products and other minerals. MMTC also has a wholly owned subsidiary named

MMTC Transnational Pte Ltd (MTPL), Singapore and various joint ventures

including a pig iron plant in which MMTC holds 49.8% stake.

Investment arguments

Mineral exports to remain muted: The developments such as ban on iron ore

mining and export from Karnataka, regulation of export from eastern sector,

increase in railway freight and higher export duty for exports, increase in

domestic demand of ore iron ore etc have resulted in lower exports of iron ore in

India during FY2012. As per Federation of Indian Mineral Industries (FIMI), iron

ore exports from India had declined by 38.5% yoy to 62mn tonnes during

FY2012 on account of export ban in Karnataka, stringent measures in issuing

export permits in Odisha, a sharp decline in international iron ore price and

increased export duty. Further, as per FIMI, total iron ore exports during FY2014

are estimated to decline significantly, thus affecting top-line of MMTC.

The

increase in domestic steel production capacity has also reduced the availabilit

y

of Chrome and Manganese Ore for exports. Moreover, export duty on chrome

ore has increased beginning March 2012 from `3,000/tonne to 30% ad

valorem; all these factors are likely to impact MMTC’s sales volumes going

forward. Even gold imports into India are likely to be lower due to increase in

customs duty on gold by the government. This is further likely to hit MMTC’s top-

line going forward.

Historical financials highly volatile: The company’s financial performance has

been inconsistent and erratic over the past few years. During FY2012, its

consolidated net profit declined by 62.0% yoy to `43 cr. During FY2013, it

reported a net loss of `71cr on a standalone basis. (The company has not

reported consolidated FY2013 results). The past financials of the company do not

indicate stability in earnings going forward.

Valuation: MMTC is a trading company with a 'Five Star Export House' status.

However, at the current price, the stock is trading at a very expensive valuation o

f

398x FY2012 PE due to low free float (0.67% of its market cap). Even at a floo

r

OFS price of `60, it is trading at FY2012 PE of 113x, which is very expensive in

our view. Hence, we recommend investors to AVOID subscribing to MMTC OFS.

Bhavesh Chauhan

Tel: 022- 39357800 Ext: 6821

V

inay Rachh

Tel: 022- 39357600 Ext: 6841

MMTC

Expensive valuation despite huge discount

FPO

|

Metals

J

une 12, 2013

Metals

|

FPO

June 12, 2013

2

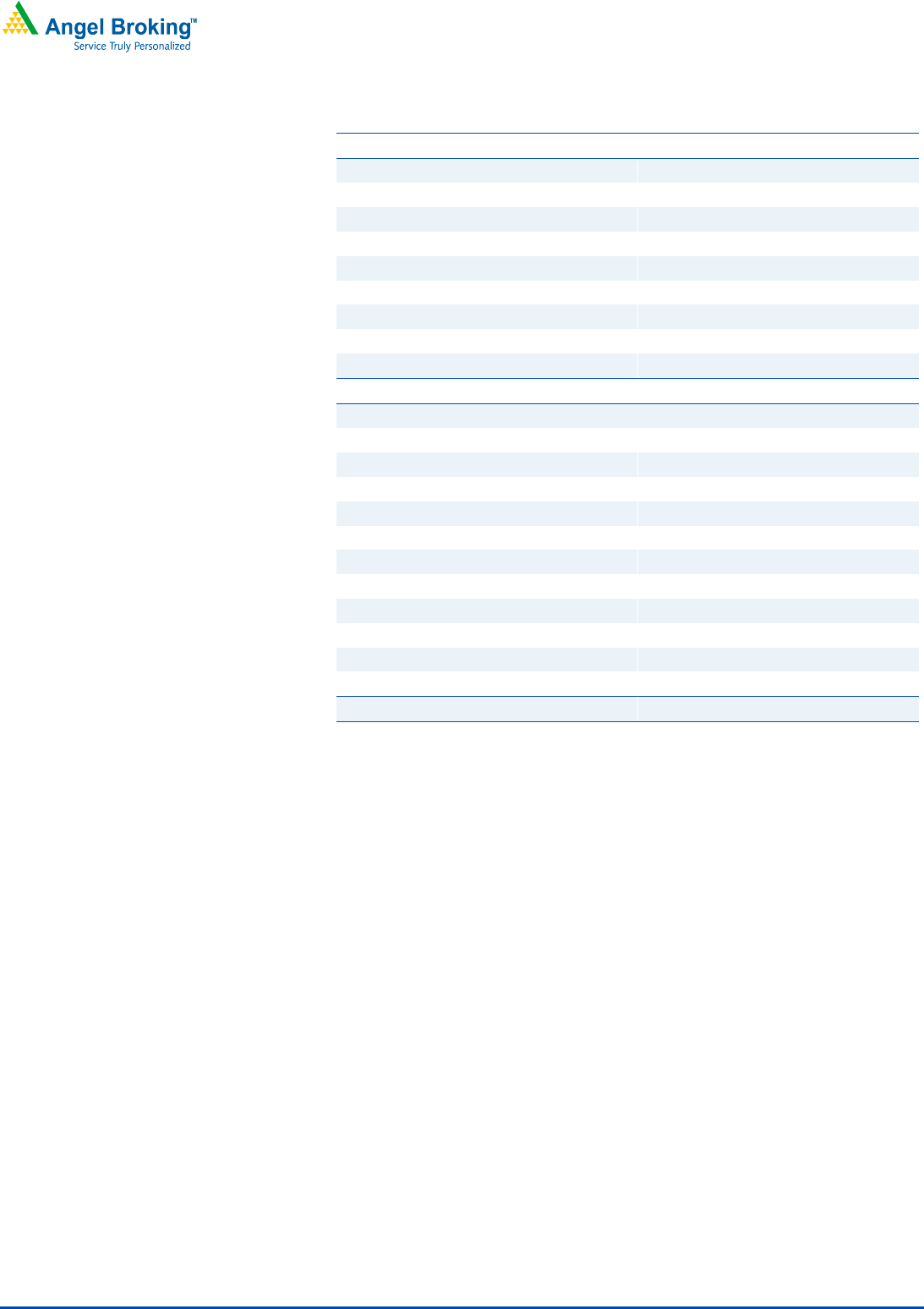

Profit & loss statement (Consolidated)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012

Net Sales

37,832 45,614 69,613 67,022

% chg

39.7 20.6 52.6 (3.7)

Total Expenditure

37,728 45,503 69,527 67,078

EBIDTA

104 111 86 (56)

(% of Net Sales)

0.3 0.2 0.1 -0.1

Other Income

841 669 510 709

Depreciation & Amortisation

13 14 14 14

Interest

687 416 399 590

PBT

245 350 184 49

(% of Net Sales)

0.6 0.8 0.3 0.1

Extraordinary Expense/(Inc.)

- - - -

Tax

81 120 71 6

(% of PBT)

33.1 34.1 38.8 13.1

PAT

164 231 112 43

% chg

(21.1) 40.7 (51.4) (62.0)

Adj. PAT

231 250 29 103

% chg

(21.6) 8.0 (88.3) 252.8

Metals

|

FPO

June 12, 2013

3

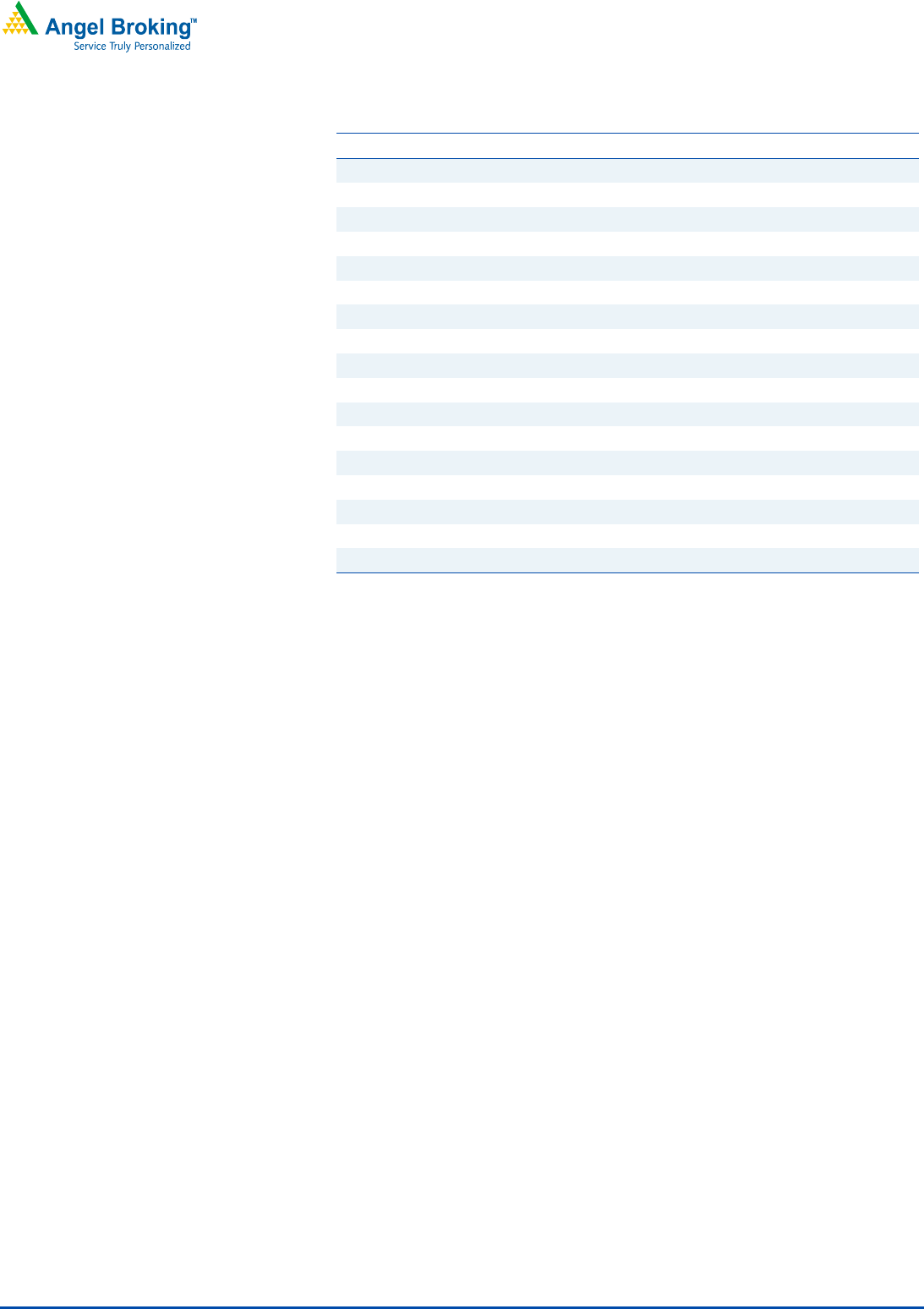

Balance sheet (Consolidated)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012

SOURCES OF FUNDS

Equity Share Capital

50 50 100 100

Reserves & Surplus

1,333 1,519 1,467 1,596

Shareholders’ Funds

1,383 1,569 1,567 1,696

Share warrants

- - - -

Minority Interest

- - - -

Total Loans

4,327 5,240 6,225 3,558

Other Liabilities

- - 130 148

Deferred Tax Liability (net)

(30) (22) (34) (71)

Total Liabilities

5,679 6,787 7,889 5,331

APPLICATION OF FUNDS

Gross Block

215 227 225 261

Less: Acc. depreciation

73 85 97 110

Net Block

142 142 128 151

Capital Work-in-Progress

21 90 134 118

Goodwill

- - - -

Investments

388 440 518 608

Current Assets

10,103 11,482 18,853 12,175

Current liabilities

4,980 5,367 11,857 7,837

Net Current Assets

5,123 6,115 6,995 4,338

Other assets

- - 114 117

Misc Expenditure

6 - - -

Total Assets

5,679 6,787 7,889 5,331

Metals

|

FPO

June 12, 2013

4

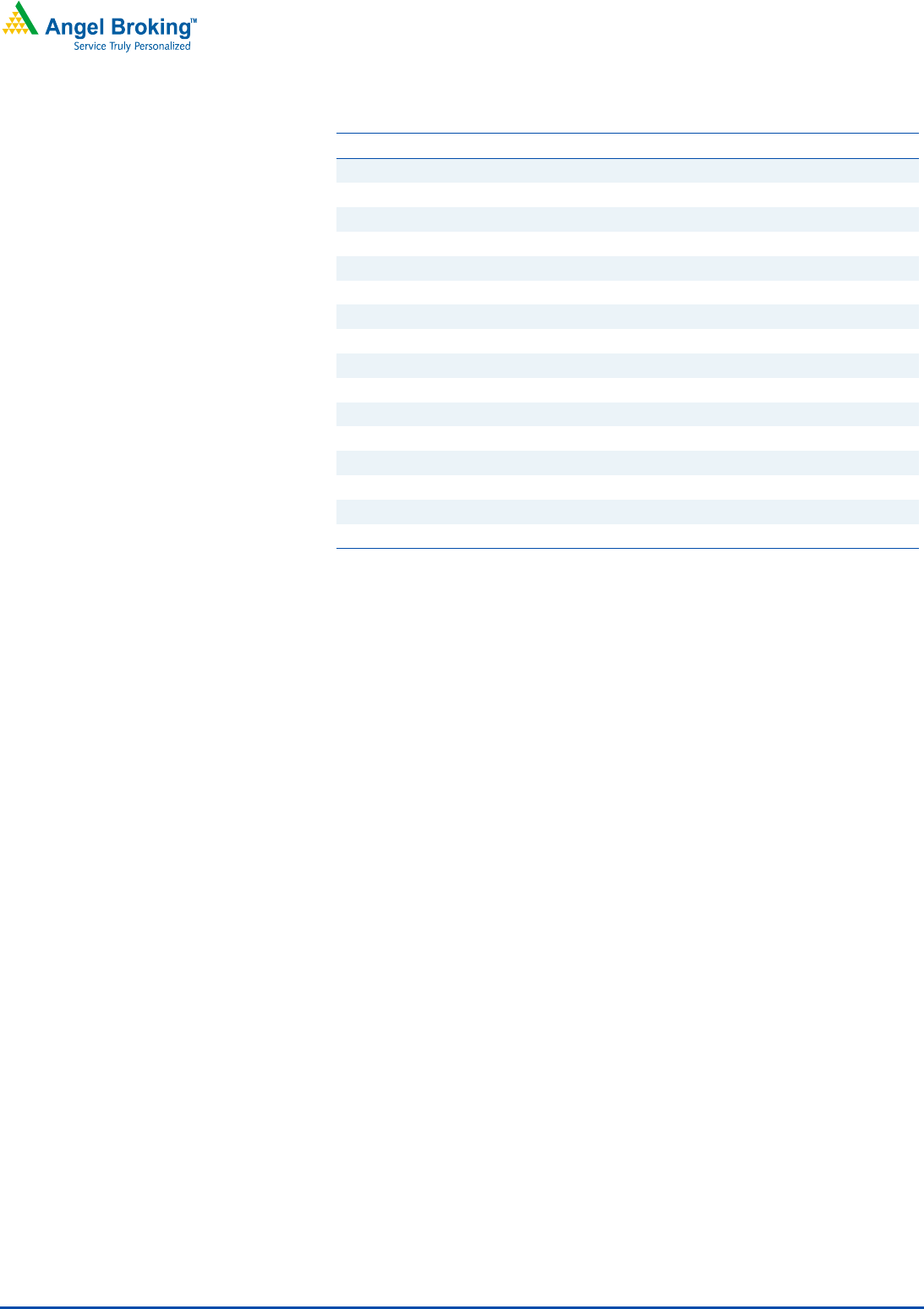

Cash flow statement (Consolidated)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012

Profit before tax

245 350 184 149

Depreciation

13 14 14 14

(Inc)/Dec in Working Capital

(1,326) (743) (181) (1,178)

Direct taxes paid

(108) (79) (92) (32)

Others

(68) (255) (92) (196)

Cash Flow from Operations

(1,243) (712) (168) (1,242)

(Inc.)/Dec. in Fixed Assets

(33) (83) (48) (22)

Free Cash Flow

(1,211) (629) (120) (1,220)

(Inc)/Dec in Investments

0 0 0 0

Others

(686) (415) (399) (591)

Issue of Equity

0 0 0 0

Inc./(Dec.) in loans

1,122 912 987 (2,666)

Dividend Paid (Incl.Tax)

(55) (23) (52) (29)

Cash Flow from Financing

381 474 535 (3,286)

Inc./(Dec.) in Cash

(58) 213 657 (3,887)

Opening Cash balances

6,022 5,965 6,178 6,835

Closing Cash balances

5,965 6,178 6,835 2,948

Metals

|

FPO

June 12, 2013

5

Key Ratios

Y/E March FY2009 FY2010 FY2011 FY2012

Per Share Data(`)

EPS (diluted)

39.4 48.5 0.2 0.5

Book Value

138.3 156.9 78.3 84.8

Ratios

EBITDA margin (%)

0.3 0.2 0.1 -

Adj. Net margin (%)

0.6 0.5 0.04 0.2

Net Debt/Equity

(1.5) (0.9) (0.7) 0.0

Returns %

RoE

15.5 17.9 9.1 8.4

RoCE

19.2 12.6 8.3 12.0

RoIC

- 37.98 10.94 -

Valuation Ratio (x)

P/E

2 1 273 113

P/BV

0.4 0.4 0.8 0.7

EV/Sales

0.0 0.0 0.1 -

EV/EBITDA

9.4 14.6 56.5 -

Metals

|

FPO

June 12, 2013

6

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report

.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement MMTC

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to -15%) Sell (< -15%)

Note: We have not considered any Exposure below

`

1 lakh for Angel, its Group companie

s

and Directors